Mount Milligan is a copper-gold mine located in British Columbia, Canada, 115 km northeast of Prince George. Mount Milligan is a porphyry-type deposit situated in the Quesnel terrane, a belt of volcanic arc and oceanic terrains, part of the North American Cordillera. The area was first prospected in 1937 and drilling in the 1980s led to the discovery of copper-gold mineralization. In 2010, Thompson Creek Metals acquired the project and constructed Mount Milligan, which commenced commercial production in 2014. Thompson Creek was acquired by Centerra in 2016 and is now a fully owned subsidiary of Centerra. Since the start of commercial production, Mount Milligan has produced 140 Mt ore, producing 561 M lbs copper and 1.6 Moz gold.

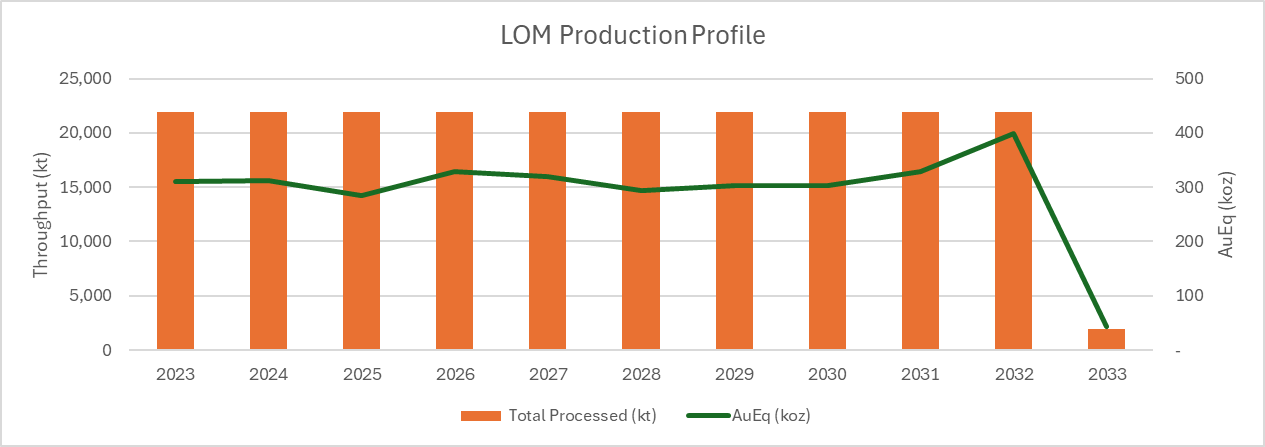

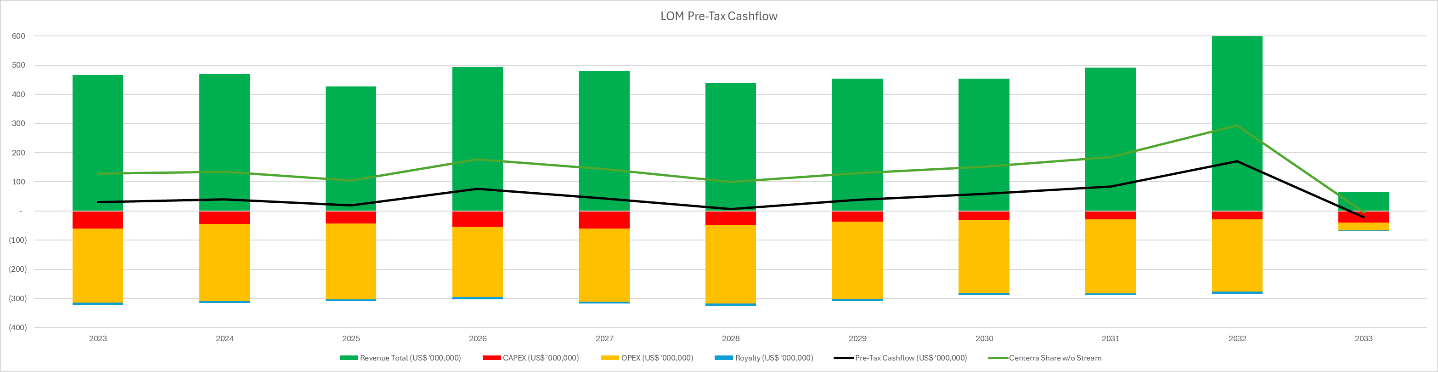

Mount Milligan is a conventional shovel and truck open pit operation with a nameplate mill throughput of 60,000 tpd. The pit is planned with a series of seven pushbacks, scheduled to conclude in 2032 with stockpile processing until 2033. LOM strip ratio is very low, at just 0.88. 221 Mt is processed, containing 2.1 Moz gold and 716 M lbs copper. Mining Momentum replicated and adjusted the cashflow presented in the Technical Report to match the LOM plan from 2023 to 2033, excluding 2022. This adjusted cashflow has a pre-tax cashflow of US$549 M and pre-tax NPV10% of US$301 M. NPV is a fairly insignificant measure for an operating mine which has no significant capital expansion plan. What is of greater importance is the annual cashflow and the years of mine life remaining, which in the case of Mount Milligan, is plenty.

| Tonnes (Mt) | Cu (%) | Au (g/t) | Cu (M lbs) | Au (Moz) | |

|---|---|---|---|---|---|

| Reserve | 246.2 | 0.18 | 0.37 | 996 | 2.9 |

| M+I | 189.3 | 0.18 | 0.30 | 742 | 1.8 |

| Inferred | 4.6 | 0.07 | 0.47 | 7 | 0.1 |

Mining Momentum has identified two key drawbacks of Mount Milligan. The first is environmental risk, namely over 70% of waste is Potentially Acid Rock Generating; it may be operationally challenging to source sufficient quantities of inert rock to encapsulate the acid-generating material. Other mitigation tools may include in-pit dumping, limestone neutralization, and more sophisticated engineering controls, but all these come at a financial cost and/or operational efficiency. Furthermore, US$39 M closure cost appears low. Even $0.50/t processed would result in triple the sum. That being said, the costs are at the end of mine life and have a reduced impact on NPV, especially with mine life extension, which will be discussed later. The second issue with Mount Milligan is its Royal Gold stream. This is not so much a risk, but rather, a fact. Take year 2028 as an example, the Centerra portion of cashflow drops to less than $10 M. Overall the Royal Gold stream removes 64% of income. Without the stream, the Mount Milligan generates a pre-tax cashflow of US$1,546 M and pre-tax NPV10% of US$902 M. The saving grace is, gold is not trading at US$1,500/oz and copper is no longer US$3.25/lb.

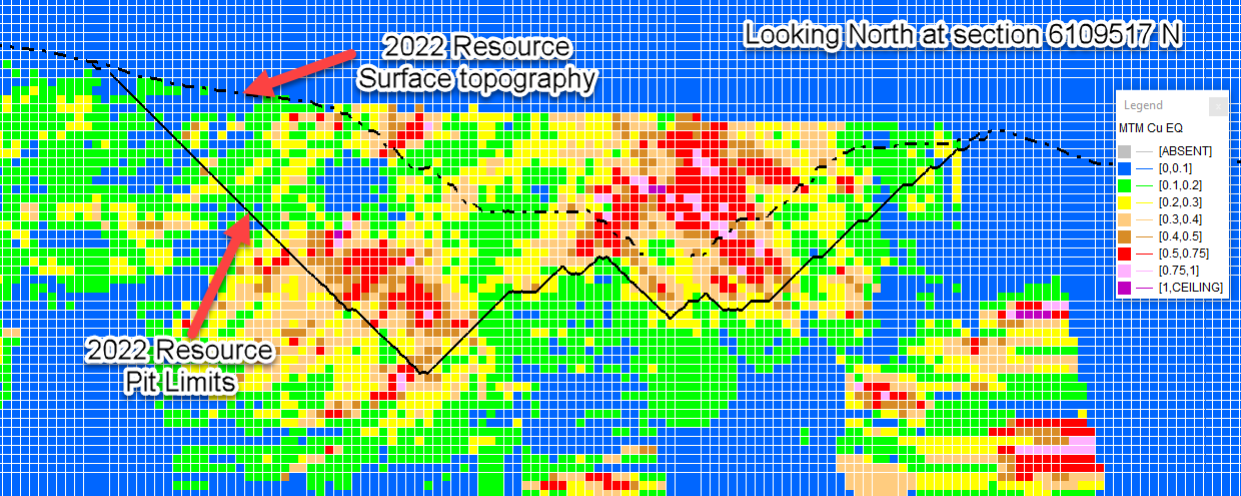

Mount Milligan is an excellent deposit. It achieves stable throughput for the next decade of LOM, steadily producing 300 koz gold equivalents. Mount Milligan does not achieve the coveted 500 koz Tier 1 badge of honour, but it is a solid mine that churns out ounces in a predictable manner. Steady state production also means that the site has the opportunity to continuously improve productivity and develop a good understanding of how the deposit behaves. Bullish metal prices also encourage conversion of Resources into Reserves. Based on information contained in the Technical Report, Mining Momentum believes the Resource is well-supported. Having already been pit-constrained, the M+I portion is ready for conversion into Reserves, which should add another seven to ten years of mine life. Furthermore, while it has yet to be declared as Resources, judging by the section view, there is strong potential to extend pit limits east and west. Additional underground potential also exists. Mining Momentum would hardly be surprised to see Mount Milligan operate past 2050!

The information presented above does not constitute investment advice. This is a summary from the NI 43-101 Technical Report effective December 31, 2021 (INSERT), with commentary from the author. Statements above do not represent the views of Centerra Gold. If any discrepancies arise, the information contained within the NI 43-101 are official and final. For latest depletion data, please refer to the AIF update.