Inkai is a uranium mine located in the Suzak District, South Kazakhstan Oblast, Kazakhstan. The deposit is hosted in sedimentary rocks of the Chu-Sarysu Basin. Inkai is situated in a uranium rich area, contiguous with South Inkai owned by Southern Mining and Chemical Company, 70% owned by Uranium One and 30% owned by Kazatomprom. Commercial production at Inkai commenced in 2009, and in total, the operation has produced 42.3 M lbs U3O8 of which 24.8 M lbs was allocated to Cameco. Inkai was previously 60% owned by Cameco and 40% owned by Kazatomprom; the Kazakh entity recently increased investment in the project, resulting in Kazatomprom’s stake increased to 60%, hence this updated NI 43-101 report.

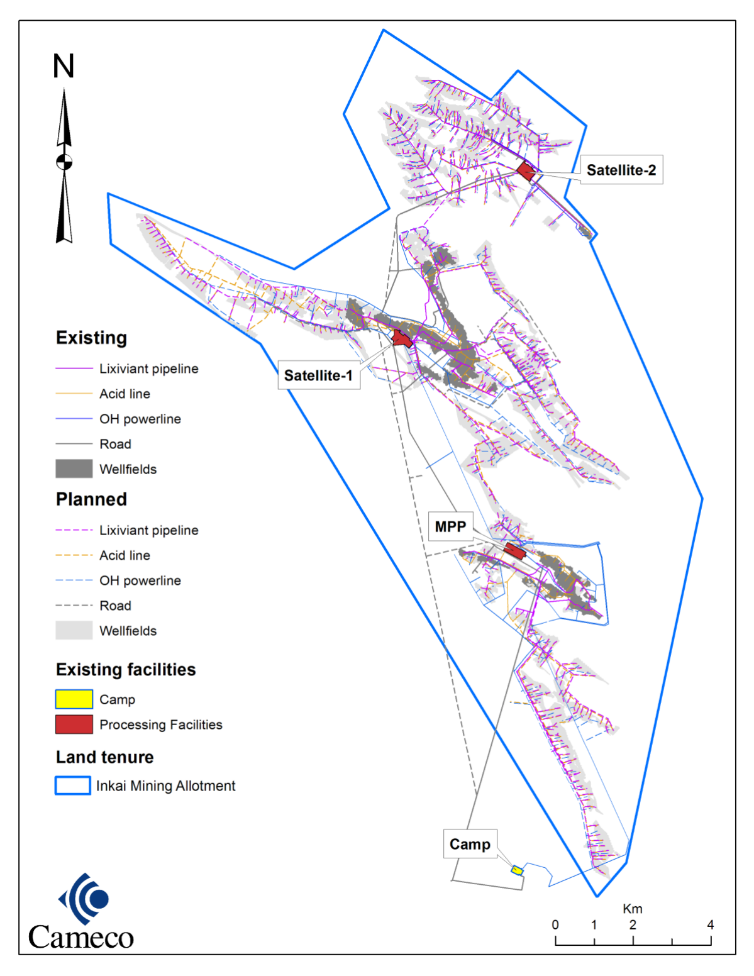

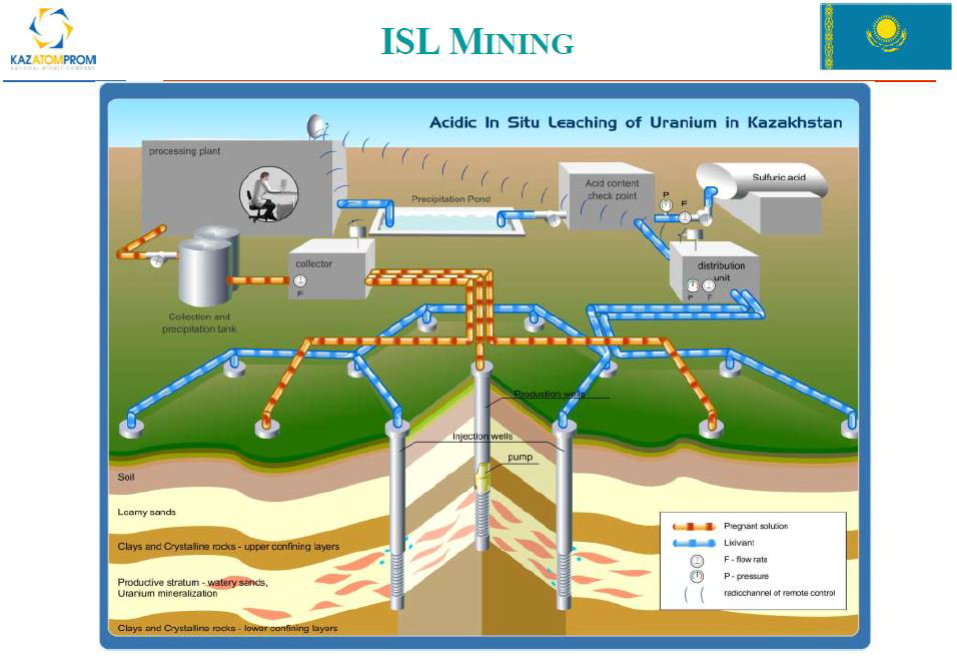

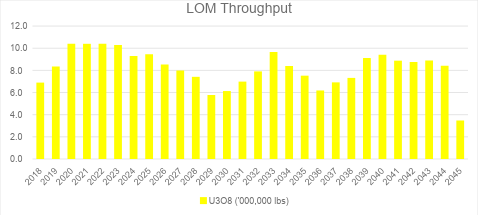

Inkai uses the In-situ Recovery (ISR) method. This is a method of extraction where a pattern of production and injector wells are drilled from surface. An acid leach solution is injected into the injection well, which then leaches the uranium ore, and is pumped up the production well. The study of hydraulic conductivity is especially important and care must be taken when designing the pattern of wells. The wells are connected to processing facilities using a network of pipes for barren and pregnant solutions. Inkai has three surface processing facilities currently operating at 5.2 M lbs per year, to be increased to 10.4 M lbs. Over life of mine, Inkai expects to produce 229.2 M lbs U3O8 to mid 2045.

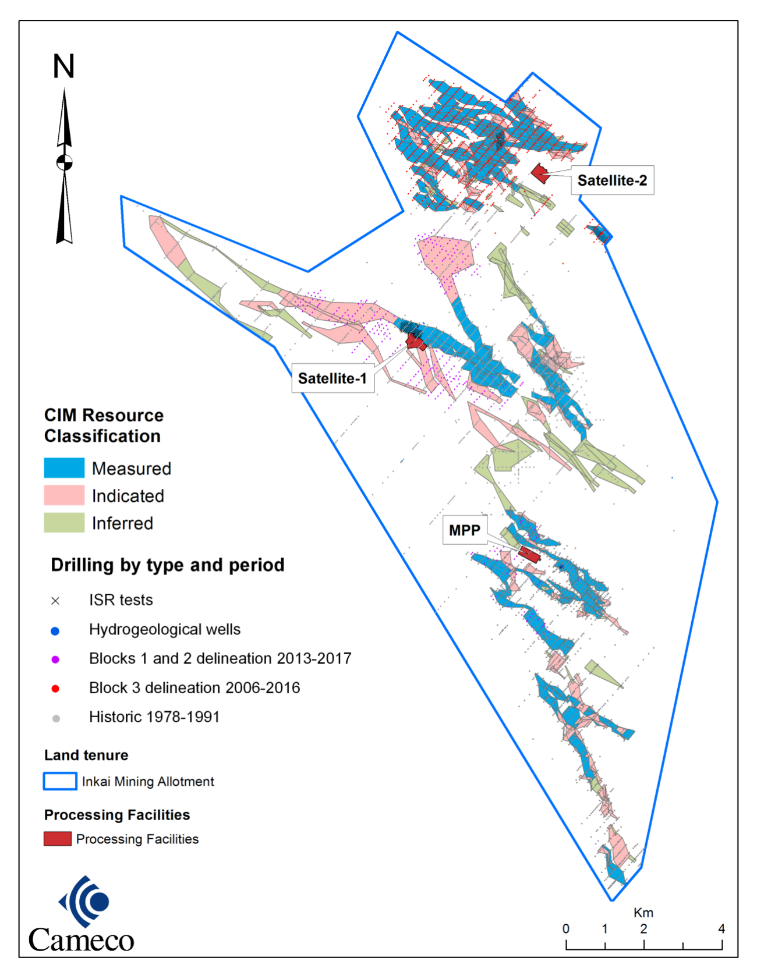

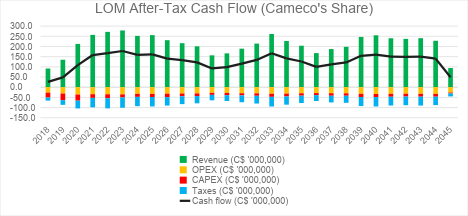

Inkai Resources and Reserves were estimated using a 2-D block model, where the z-axis (depth) has been weighted and cutoff grades are reported as m%. This method is used since extraction uses wells, hence concentration along the depth of a hole gives weight to the economic value of the contained mineral. Resources were calculated using uranium price of US$33/lb, cost of US$11.50/lb, while Reserves were calculated using a price of US$54/lb and an operating cost of $9.55/lb. 85% recovery and exchange rates US$/C$ 1.25 and Kazakhstan Tenge/C$ 265 were used. Subsequent cutoff grades are 0.047 m% U3O8 Block 1 and 0.071 m% U3O8 Blocks 2 MA and 3 MA. The project has an after-tax NPV12% C$2.2B (100% JV Inkai), after-tax IRR 27.1%; Cameco’s 40% share amounts to an after-tax NPV12% C$880 M.

| Classification | Tonnes (‘000 t) | Grade (% U3O8) | Contained (M lbs U3O8) | Cameco’s Share (M lbs U3O8) |

|---|---|---|---|---|

| Reserve | 381,017.2 | 0.032 | 269.6 | 107.9 |

| Resource (M+I) | 57,813.2 | 0.025 | 32.0 | 12.8 |

| Inferred | 116,394.6 | 0.029 | 75.0 | 30.0 |

With over two decades of remaining mine life, the focus of Inkai is on upgrading and increasing production over exploration. It is worth highlighting that Inkai Resources have more conservative economic parameters than Reserves. The Resource inputs were defined by the parameters used in the TEO study, a technical and economic evaluation based on permanent conditions, required by Kazakh authorities. This largely explains why very little material reports to M+I Resource. Inferred Resources require additional infill drilling to move into M+I Resource and subsequent evaluation for P+P Reserve. This likely contains an additional five to ten years of mine life. Operations are experienced with the ISR method and its characteristics are well understood. With elevated uranium prices and many years of mine life, Inkai provides a stable and financially secure source of uranium.

The information presented above does not constitute investment advice. This is a summary from the NI43-101 Technical Report effective Jan 1, 2018 (INSERT), with commentary from the author. Statements above do not represent the views of Cameco. If any discrepancies arise, the information contained within the NI43-101 are official and final. For latest depletion data, please refer to the AIF update.