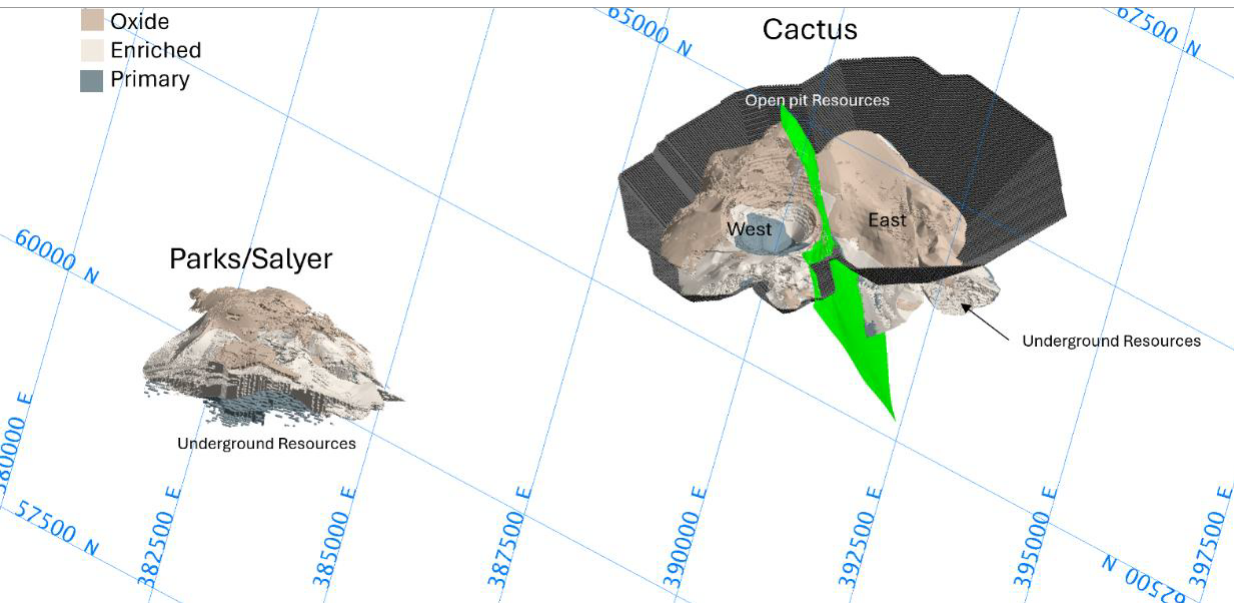

The Cactus Project is located in Arizona, USA, 40 miles southeast of Phoenix. The Cactus Project consists of Cactus West and Cactus East, located at the historic Sacaton mine, and Parks/Salyer located to the west. The Project occurs in the desert region of the Basin and Range province of Arizona, an area characterized by intrusion, deposition, erosion, fracturing, faulting, brecciation, and alteration. The deposits are part of a large porphyry copper system which have been dismembered and displaced by faulting and display typical characteristics of a porphyry copper deposit. Sacaton was first discovered in the 1960s by ASARCO geologists. An open pit operated between 1974 and 1984, extracting 38.2 Mtn of ore, producing 199 tn of copper, 27.5 koz of gold, and 759 koz silver. A 2,000 ft shaft was sunk east of the pit, but underground mine development was suspended in 1981 due to unfavourable copper prices. Parks/Salyer was first drilled in 1976 and additional drilling was carried out but the exploration target was not advanced further. In 2020, Arizona Sonoran completed the purchase of the property from the custodial trust responsible for managing the site.

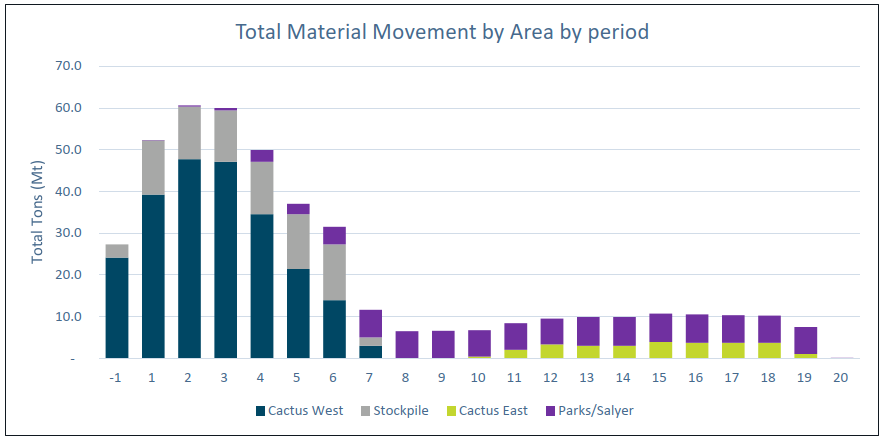

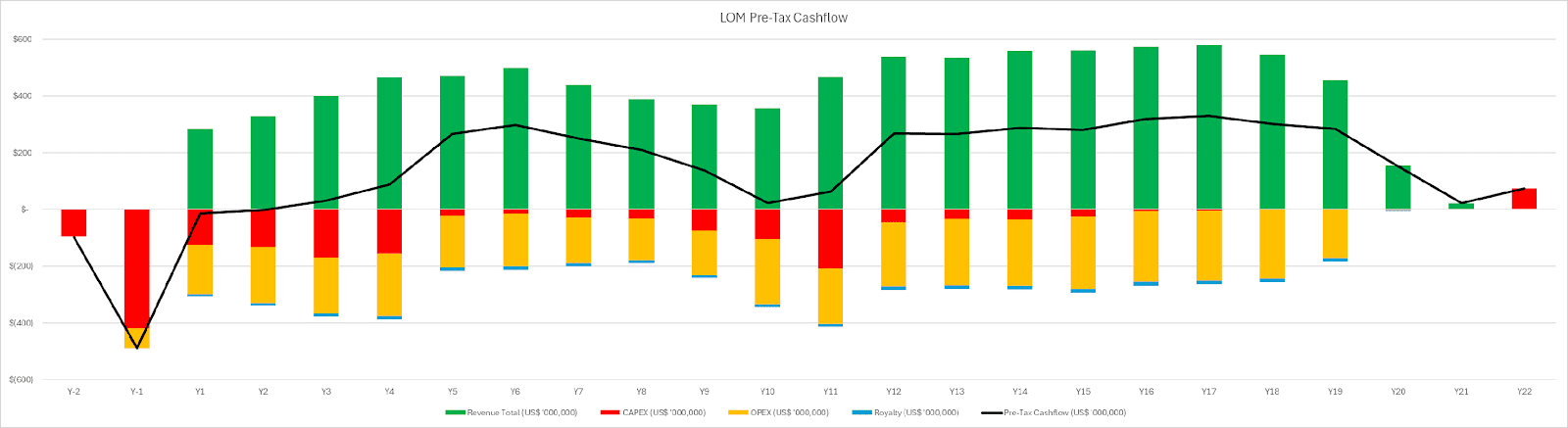

Mining is planned to start as an open pit operation at the historic Sacaton pit in conjunction with processing existing stockpiles. As open pit operations wind down, underground mining commences at Parks/Salyer. Underground mining at Cactus East begins after open pit mining has been completed. Open pit mining is planned as a conventional shovel and truck operation. Due to the limited size of the pit, production does not maintain steady state. Phase 1 ramps up to 13 Mtn ore before winding down and Phase 2 reaches 18 Mtn ore. Overall, the Reserve pit extracts 75 Mtn ore at a strip ratio of 1.9. 12 Mtn stockpile ore is processed per year during open pit operations. The underground is envisaged as a sublevel cave operation with a planned production rate of 10 Mtn per year. Ore is planned for processing as heap leach. Per the Technical Report, pre-tax NPV8% is US$733 M with an IRR of 17.7% with a payback period of just over 6 years.

| Tons (M tn) | Grade Cu (%) | Contained Cu (M lbs) | |

|---|---|---|---|

| Reserve | 276.3 | 0.55% | 3,031.2 |

| Cactus OP | 75.5 | 0.31% | 463.7 |

| Stockpile | 76.8 | 0.16% | 250.3 |

| Cactus UG | 27.7 | 0.95% | 527.0 |

| Parks/Salyer UG | 96.2 | 0.93% | 1,790.2 |

| M+I | 445.7 | 0.58% | 5,174.0 |

| Cactus OP | 220.3 | 0.42% | 1,868.0 |

| Stockpile | 71.0 | 0.15% | 217.3 |

| Cactus UG | 10.4 | 0.88% | 183.5 |

| Parks/Salyer UG | 143.9 | 1.01% | 2,906.1 |

| Inferred | 233.8 | 0.47% | 2,207.9 |

| Cactus OP | 177.9 | 0.33% | 1,167.0 |

| Stockpile | 1.2 | 0.13% | 3.0 |

| Cactus UG | 6.4 | 0.78% | 100.1 |

| Parks/Salyer UG | 48.4 | 0.97% | 936.1 |

Mining Momentum recognizes the complexity of planning and sequencing the various orebodies at the Cactus Project. The Life of Mine plan contained in the Technical Report essentially uses a starter pit to finance underground mine development. Mining Momentum identified a number of issues with the Cactus Project which are highlighted below:

- Underground mining at the Cactus Project is more profitable than open pit mining. Placing underground mining at the latter years of the production sequence increases discounting. Using CAPEX spend in Years 9 to 11 and removing Revenue, NPV8% exceeds US$1 B, higher than the entire project value contained in the PFS. This effect is even more pronounced if a higher discount rate is used.

- As a caving operation, underground mining at Cactus cannot begin until open pit operations have ceased. This constraint causes a lull in production profile.

- Operations at Cactus are complex, requiring separate fleets for Cactus open pit, stockpiles, Cactus underground, and Parks/Salyer underground, increasing capital expenditure and reducing operational efficiency.

- Open pit operations are small in scale, ramp up, and wind down, never reaching full operational efficiency of steady state mining.

- G&A costs appear low, US$3.2 M per year open pit and US$1.2 M per year underground. Amount could be 10x.

- Closure cost appears low and salvage value is not likely to be realized for a high throughput, long-life project. The credit of US$74 M at the end of mine life as shown in the PFS is likely to manifest as a spend in excess of US$250 M. Although this number appears large, due to the length of the project, the effects of discounting somewhat reduces its impact.

- Contingency is low, sitting at 16% compared to 15%-25% recommended by AusIMM and 15%-30% recommended by SME. A US$200 M cost overrun is not unexpected.

Mining Momentum recognizes that a large amount of work has been completed to demonstrate feasibility of the Cactus Project. However, we are of the opinion that certain costs remain outstanding and represents downside risk to project value. Factoring these costs in, the project appears economically marginal. Without accessing the block model and performing an in-depth analysis, Mining Momentum believes project value may actually increase if evaluating the Cactus Project as purely underground operations. Mining Momentum also highlights the large discrepancy between the current Reserve pit and Resources. Just 25% of open pit M+I Resources has been converted to Reserve, with an additional 178 Mtn classified as Inferred. This material may be unrecoverable once underground caving begins, placing 3 B lbs copper at risk. Mining Momentum recommends taking a serious look the possibility of a larger pit and undertaking increased drilling to reclassify the open pit Inferred material. Assuming 75% M+I and 50% Inferred conversion, this could become a multi-decade pit with 330 Mtn ore containing 2.4 B lbs copper.

The information presented above does not constitute investment advice. This is a summary from the NI 43-101 Technical Report effective February 21, 2024 (INSERT), with commentary from the author. Statements above do not represent the views of Arizona Sonoran. If any discrepancies arise, the information contained within the NI 43-101 are official and final. For latest depletion data, please refer to the AIF update.