Cayeli is an underground copper-zinc mine located in Turkey, 7.5 km east of the port town of Rize. The deposit is a massive sulphide orebody situated in the Pontid volcanic belt. The mineralization has a Measured Resource with strike length of 600 m, vertical depth over 600 m, average thickness of 20 m, and average dip of 65 degrees. Near mine exploration has been limited and the deposit remains potentially open at depth. Mining activities in the area date back over a millennium and by the first half of the 20th Century, various shafts and adits were driven along with small scale production. In 1967, the Turkish Mineral Research and Exploration Institute carried out exploration activities in the area, resulting in construction in 1992 and commercial production in 1994. At the time of publication of the Technical Report, the mine has been in operation for 11 years, mining 8.76 Mt ore to produce 378 kt copper and 519 kt zinc.

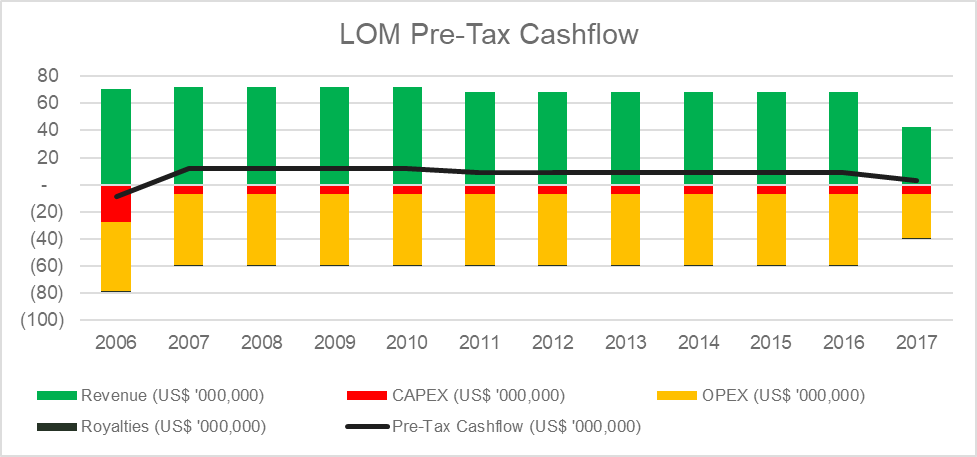

The deposit is divided into Main and Deep Zones, delineated by the Scissor Fault. The underground is accessed via ramp and material is skipped to surface via shaft. The mine operates at an average throughput of 800 ktpa, slated to increase to 1 Mtpa with the shaft deepened to 600 m. Most of the deposit is mined as transverse longhole and the rest mined as longitudinal longhole. A primaries/secondaries sequence in transverse stopes is amenable to high productivity. Ore is processed into a copper concentrate and a zinc concentrate in a 3,600 tpd facility. At the time of publication of the Technical Report, Cayeli has an 11.6 Mt Reserve, but a mine plan exists only for the next five years. Using Reserve quantities contained in the five-year plan, Mining Momentum has extrapolated the remainder of mine life to deplete the Reserve to produce a Pre-Tax Cashflow of $95.7 M, US$51.8 M discounted 10%. This assumes an annual spend of US$7 M sustaining capital in addition to $20.6 M capital spend in the 2006 budget; closure costs have been excluded. Although OPEX was $56.61/t in 2005, Mining Momentum has kept the $52/t forecast from the Technical Report in its LOM analysis. Using recoveries of 86.05% copper and 72.12% zinc from the previous five years of operation, the remainder of mine life is expected to produce 364 kt copper and 491 kt zinc.

| Tonnes (Mt) | Cu (%) | Zn (%) | Ag (g/t) | Au (g/t) | Pb (%) | NSR ($/t) | |

|---|---|---|---|---|---|---|---|

| Reserve | 11.60 | 3.65 | 5.87 | 49 | 0.56 | 0.34 | 70 |

| M+I | 4.56 | 3.06 | 2.78 | 21 | 0.46 | 0.16 | 55 |

| Inferred | 1.07 | 3.34 | 6.29 | – | – | – | – |

| Tonnes (Mt) | Cu (kt) | Zn (kt) | Ag (koz) | Au (koz) | Pb (kt) | |

|---|---|---|---|---|---|---|

| Reserve | 11.60 | 423 | 681 | 18,277 | 209 | 39 |

| M+I | 4.56 | 140 | 127 | 3,079 | 67 | 7 |

| Inferred | 1.07 | 36 | 67 | – | – | – |

Cayeli has been in production for over a decade and operational characteristics are well known. Mining Momentum is of the opinion that Cayeli is a deposit with huge potential and that not all opportunities have been exploited, some of which will be discussed briefly below:

- Stopes are wireframed rather than using stope optimizer software. Opportunities exist in optimizing stope economics, especially in areas where a halo exists in place of a defined contact.

- 4.5% dilution and 92.5% extraction initially appears optimistic but block model reconciliation has been excellent (+1.1%/-0.1%).

- Stopes are small (5,000 t to 8,000 t each) and stope design studies should be carried out to improve stope cycle productivity.

- Limited orebody strike length increases lateral development demands. Stope cycle productivity is reduced and increases dependence on capital development lead. Average development demand of 11.3 m/d is easily achieved with Cayeli’s fleet of four jumbos.

- Ramp designs are not optimized for haulage efficiency.

- Issues with ground conditions may be alleviated by 3-D stress modelling and sequencing.

- Ore sills are currently 7-10 m wide; reduction in drifts spans will reduce cost and increase stability.

- Mill currently has excess capacity. 3,600 tpd should be achievable with Cayeli’s fleet of three to four drills, two V-30 machines, and eight LHDs.

- Risk exists in rising OPEX. Resource cutoff is $35/t, Reserve cutoff is $46/t, and forecasted OPEX is $52/t; meanwhile 2005 actuals was $56.61/t. Quantity of incremental ore is not specified in the Technical Report.

In addition to operational improvements, Cayeli remains open at depth and much of the property has yet to be drilled. Using commodity prices of US$4/lb copper, US$1.3/lb zinc, US$30/oz silver, US$2,400/oz gold, and $0.90/lb lead increases NSR three-fold, to approximately US$210/t. Using Canadian and American escalations, OPEX should be in the range of US$78/t to US$104/t. A key aspect impacting costs is the TRY/USD rate, which stood at 1.32 in 2006 but ballooned to 34.25 in 2024, a highly favourable position for First Quantum. Notwithstanding foreign exchange rates, profit margins have improved from US$18/t in 2006 to well over US$100/t in 2024. A new study should be undertaken to remodel the deposit at Cayeli and fully capture the operational opportunities that exist.

The information presented above does not constitute investment advice. This is a summary from the NI 43-101 Technical Report effective March 30, 2006 (INSERT), with commentary from the author. Statements above do not represent the views of First Quantum Minerals. If any discrepancies arise, the information contained within the NI 43-101 are official and final. For latest depletion data, please refer to the AIF update.