The Cobre Las Cruces Project is a polymetallic primary massive sulphide deposit situated in Seville Province, Spain, 20 km northwest of Seville. The deposit is in the eastern portion of the Iberian Pyrite Belt, known for its volcanogenic massive sulphide deposits. Mineralization was the result of metal precipitation from hydrothermal fluids, hosted by felsic volcanic rocks and black shale sedimentary rocks, buried under 100 m to 150 m of sandstone and mudstones. The deposit was first discovered in 1994 and first ore was delivered in 2009. By cessation of mining operations in 2021, 14.42 Mt ore was mined at a grade of 5.41% copper. For an additional two years, 3.5 Mt tailings were reprocessed to recover 23 kt copper. The newly proposed project plans for processing ore from a 2 Mtpa underground mine in conjunction with surface stockpile.

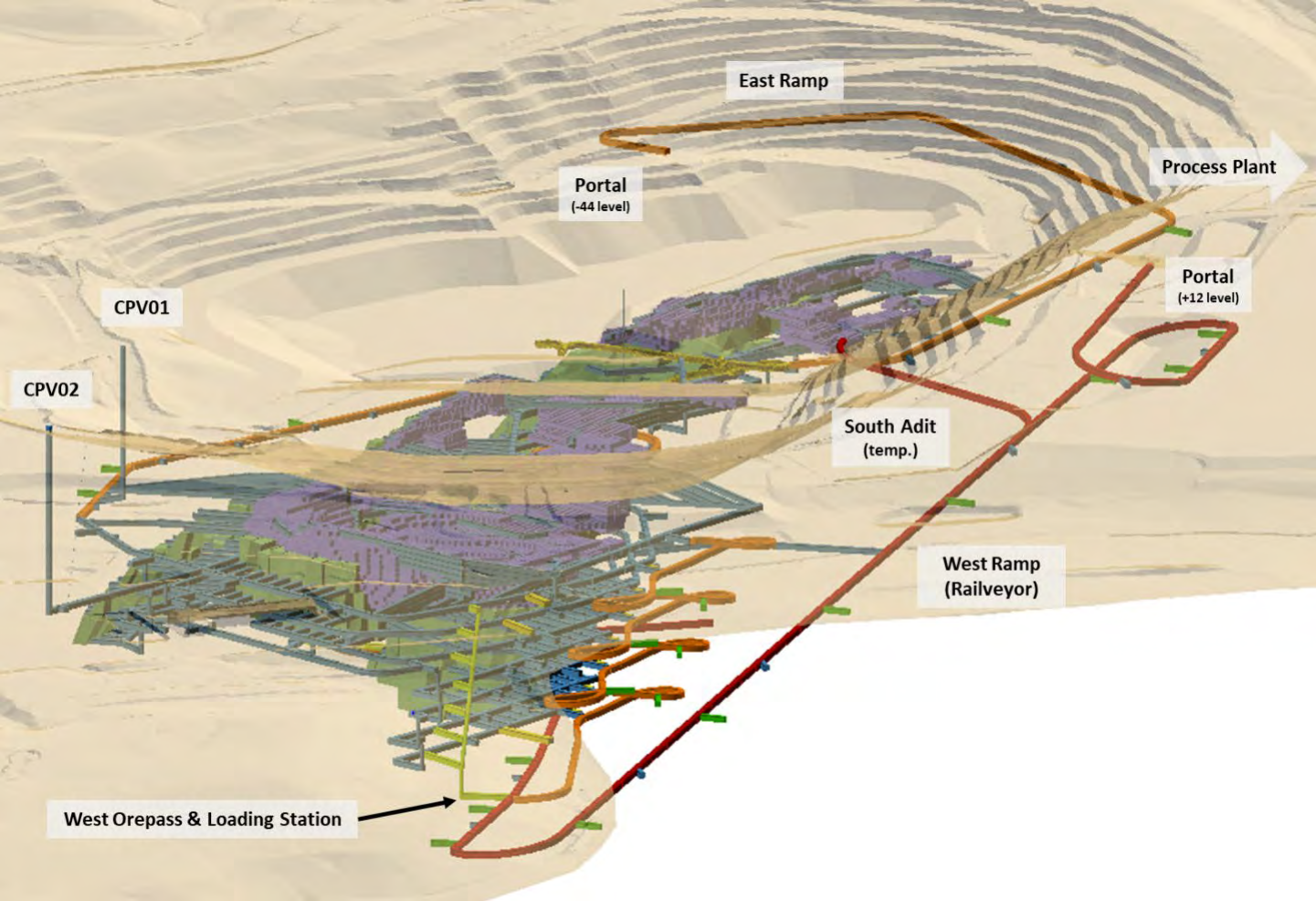

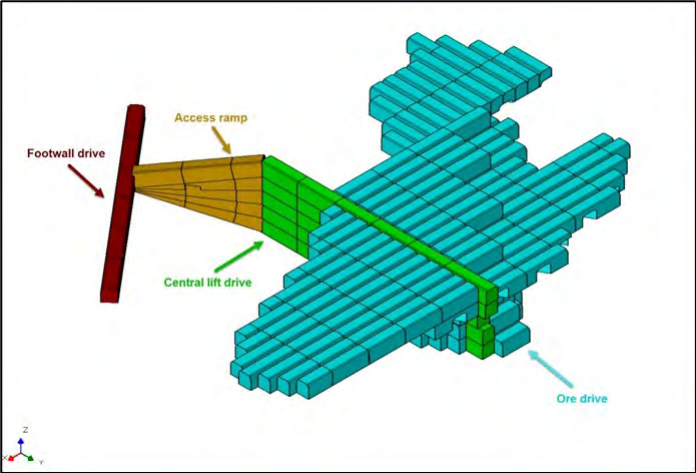

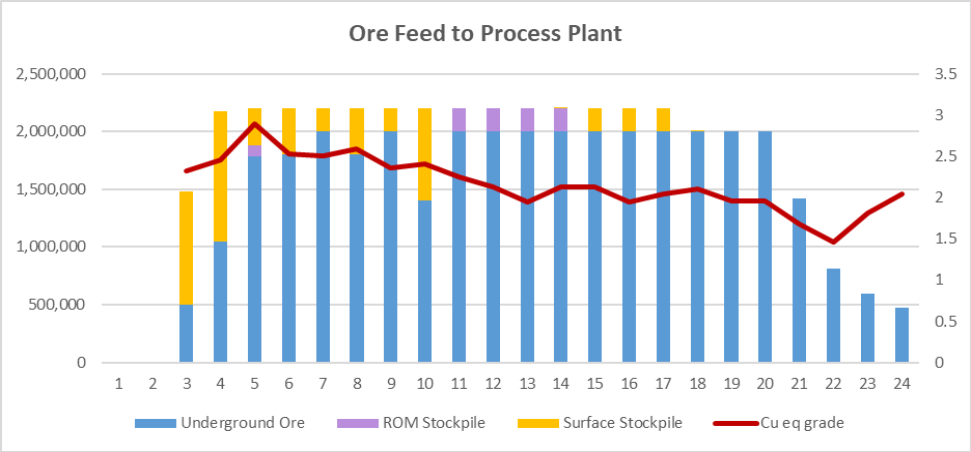

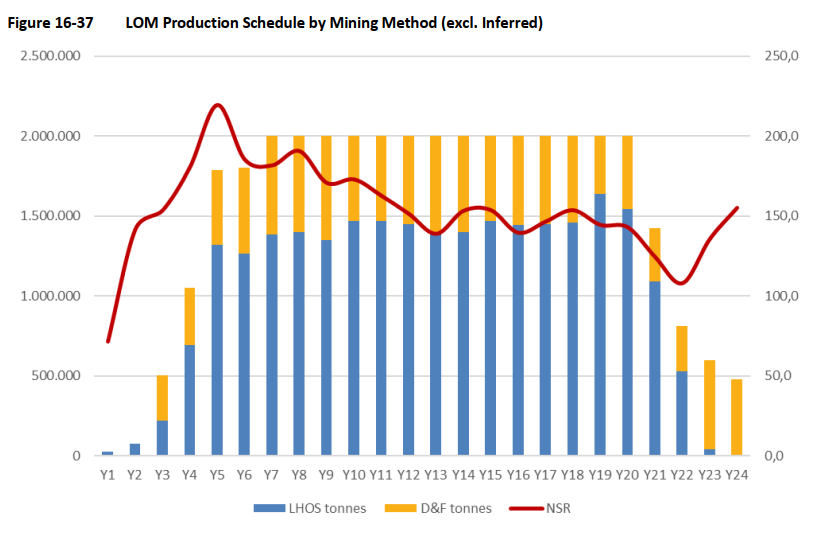

The underground mine is planned to be accessed via two declines, one located in-pit and the other on surface, which will host the Railveyor system. The Railveyor is a hybrid solution that uses cars instead of a belt in a conveyance system. Production mining is planned for transverse and longitudinal longhole and drift and fill mining. Drift and fill is used for areas where the ore is less steeply dipping and less massive. Drift and fill offers increased flexibility at the expense of reduced productivity and higher cost. Pastefill is required for primary longhole stopes and drift and fill. The mine is planned to operate at a throughput of 5,500 tpd. The first three years will be focused on underground development at a planned rate of 8,000 m/year. The project is expected to require US$846 M in pre-production capital and US$104 M sustaining capital, with operating cost at $90.25/t. A total of 403 kt copper, 342 kt lead, 790 kt zinc, and 18 Moz silver will be recovered over the 24-year mine life.

| Pre-Tax | After-Tax | |

|---|---|---|

| NPV8% (US$ ‘000,000) | 519 | 356 |

| NPV10% (US$ ‘000,000) | 392 | 257 |

| IRR | 17.4% | 15.7% |

| Optimization Inputs | Copper | Lead | Zinc | Silver |

|---|---|---|---|---|

| Price | US$3.77/lb | US$0.94/lb | US$1.21/lb | US$21.37/oz |

| Head Grade | 1.13% | 0.97% | 2.14% | 25.47 g/t |

| Recovery | 85.12% | 79.38% | 88.41% | 51.88% |

| Payable | 100% | 100% | 90% | 90% |

| Grade | Tonnes (Mt) | Cu (%) | Au (g/t) | Zn (%) | Pb (%) | Ag (g/t) |

|---|---|---|---|---|---|---|

| Reserve | 41.6 | 1.14 | 0.00 | 2.15 | 1.05 | 25.94 |

| Resource (M+I) | 8.4 | 0.86 | 0.00 | 1.83 | 0.21 | 33.06 |

| Inferred | 9.4 | 1.08 | 0.00 | 0.94 | 0.61 | 26.10 |

| Metal | Tonnes (Mt) | Cu (kt) | Au (koz) | Zn (kt) | Pb (kt) | Ag (Moz) |

|---|---|---|---|---|---|---|

| Reserve | 41.6 | 472.0 | 0.0 | 893.0 | 437.0 | 34.7 |

| Resource (M+I) | 8.4 | 72.6 | 200.5 | 154.0 | 160.1 | 8.9 |

| Inferred | 9.4 | 1.0 | 0.0 | 1.0 | 1.0 | 7.9 |

Economic analysis was completed using US$3.80/lb Cu, US$1.20/lb Zn, US$0.95/lb Pb, US$22.75/oz Ag and 95% payable for lead and silver. While the technical report cites positive project economics, several concerning aspects of the project stood out to Mining Momentum.

- 20% increase in operating cost results in NPV of zero. Risk exists since US$90.25/t is low for an operation that uses pastefill.

- 15% reduction in metal price results in an NPV of zero. Risk exists since metal prices used in this study are close to spot price.

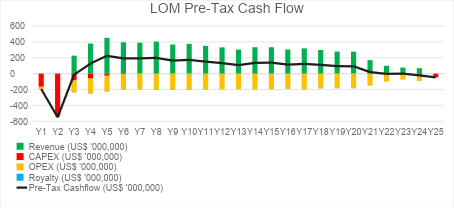

- Last five years of project life do not display positive cash flow.

- Potential exists to expedite mine plan by accelerating drift and fill mining since it does not require the development lead of longhole mining.

- Less than US$105 M is allocated to develop 70 km of tunnels. Subsequent unit cost of US$1,500/m is likely an underestimation. Three to five times the amount is typical.

- Development at the start of mine demands 22 m/d from two headings. Risk exists in achieving planned advance rate. 25%-50% of this amount is typical.

- Shallowly dipping ore may cause stability issues, risking increased dilution, increased costs from remediation efforts, and reduced productivity.

Taken in isolation, the items above may not ruin a project. However, evaluated in tandem, they point to risky project economics based on a mine plan that focuses on long life rather than optimal economics. An opportunity exists to refine the mine plan to increase its robustness in cost and executability. It may be more profitable and less risky to be more selective with mining and focus on project economics.

The information presented above does not constitute investment advice. This is a summary from the NI 43-101 Technical Report effective Sep 30, 2023 (INSERT), with commentary from the author. Statements above do not represent the views of First Quantum Minerals. If any discrepancies arise, the information contained within the NI 43-101 are official and final. For latest depletion data, please refer to the AIF update.