The following piece about Lumwana is based on the new NI 43-101 report dated February 19, 2025. You can read our original analysis of Lumwana HERE.

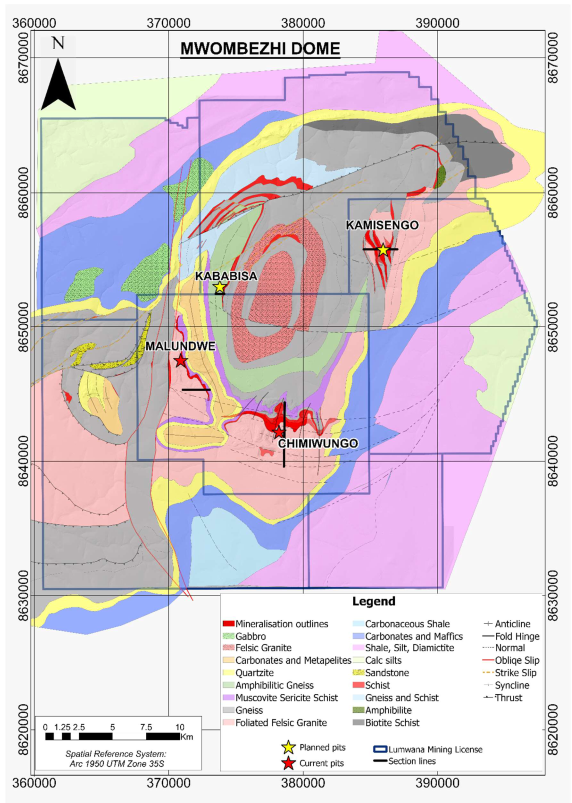

Lumwana is copper mine located in the Republic of Zambia, 400 km northwest of the capital Lusaka. Lumwana is situated in the Mwombezhi Dome, hosted in metamorphosed schists with disseminated sulphides. The area was first explored in the late 1950s eventually coming under ownership of Phelps Dodge. Equinox earned a 51% interest from Phelps Dodge in 2003 by funding a Bankable Feasibility study and acquired the remainder the following year. Barrick came to own Lumwana when it acquired Equinox in 2011. Lumwana started production in 2009 and at the time of publication of the technical report, 353 Mt ore had been processed to recover 1,845 kt copper.

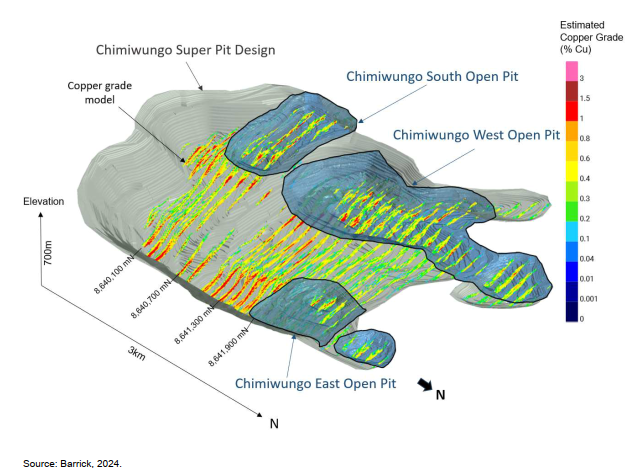

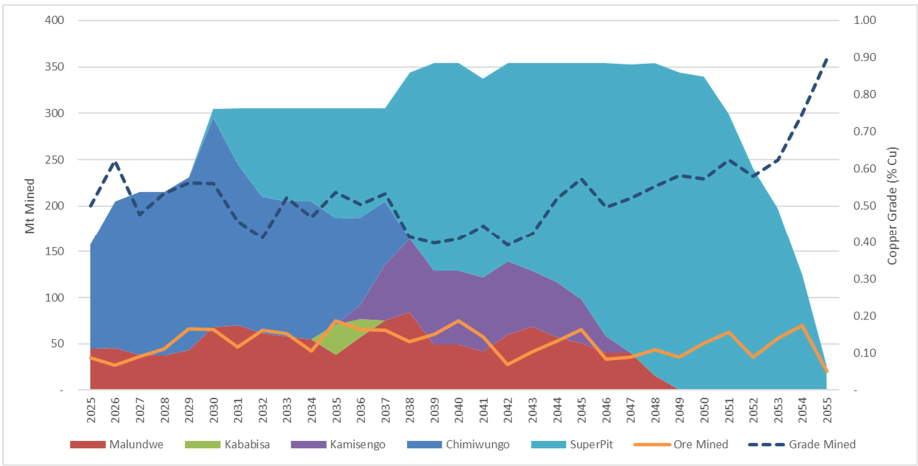

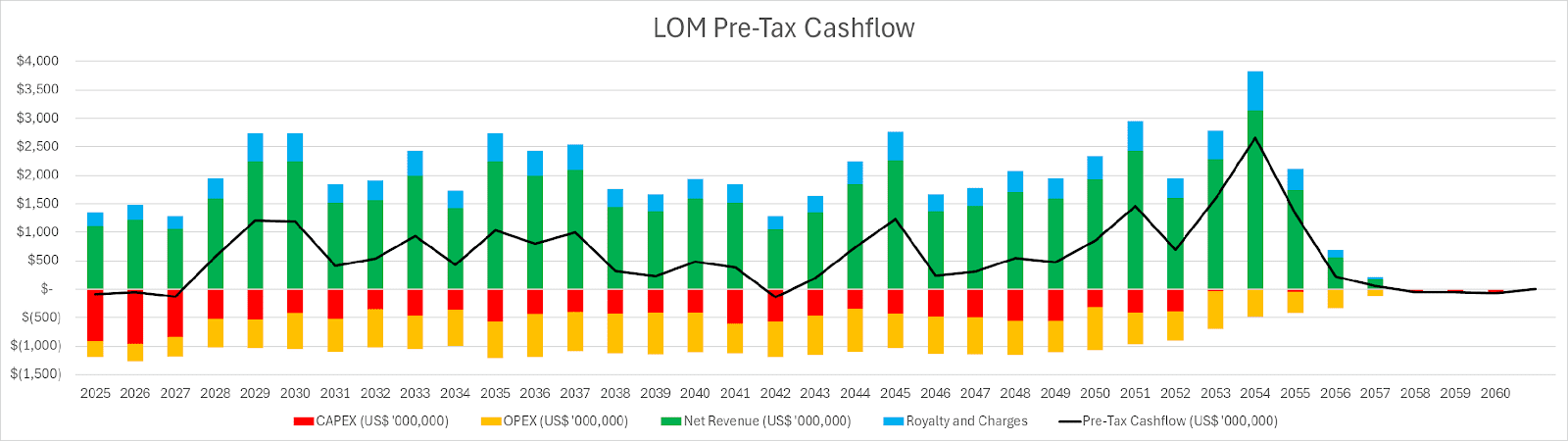

Open pit mining at Lumwana currently consists of two open pits, Malundwe and Chimiwungo. The updated Technical Report considers expansion of the three pits at Chimiwungo to be mined as a single super pit and adding two additional deposits, Kababisa and Kamisengo. Processing also ramps up from the current 25 Mtpa to 52 Mtpa. This results in a Life of Mine extension from 2038 to 2057, producing 1,592 Mt ore at a grade of 0.52% copper with 93% recovery, yielding a strip ratio of 4.7:1, up from the 2.7:1 contained in the 2013 Technical Report. Barrick reported a pre-tax cashflow of US$21.6 B, which Mining Momentum was able to reproduce to within 1.5% accuracy. Applying 8% and 10% discount rates to the cashflow results in NPVs of US$5.7 B and $4.5 B respectively.

| Tonnes (Mt) | Grade Cu (%) | Contained Cu (M lbs) | |

|---|---|---|---|

| Reserve | 1,620 | 0.52% | 18,439 |

| OP | 1,600 | 0.53% | 18,298 |

| Stockpile | 20 | 0.32% | 141 |

| M+I | 400 | 0.40% | 3,527 |

| OP | 400 | 0.40% | 3,527 |

| Inferred | 230 | 0.40% | 2,006 |

As we wrote in our previous piece, Lumwana is a solid deposit. This observation has been confirmed by the latest Technical Report, where after a decade of mining, the 25-year mine life estimated in 2013 has now been extended by a couple decades and at double the processing throughput. As described in our previous analysis, Lumwana was profitable with a small margin, but since then, copper prices have exceeded US$2.24/lb. This has provided impetus for Lumwana’s expansion. While we have presented the US$4.03/lb case, the project was planned at US$3.00/lb copper, which is expected to provide a comfortable margin to weather a copper price downturn.

Still, Lumwana exhibits several weaknesses, which Mining Momentum would like to highlight. One that comes to the forefront, is the significant cost of capitalized stripping, amounting to over a third of operating cost. While this does not necessarily impact project economics, it is somewhat unusual of a cost allocation, which may have an effect on leverage and underreport cash cost. There are also a number of years where cashflow is not particularly strong. It is apparent that the mine life extension of Lumwana was not a decision taken lightly, but rather, the result of significant tradeoff studies, whereby a much increased throughput was necessary to justify the substantial capital investment. The key takeaway here, is that material from Kamisengo and Kababisa function as the lynchpin to this endeavour. These pits are relatively small, rendering them particularly sensitive to copper price, which reduces revenue, bringing return on investment into question. This causes a cascading effect, where without Kamisengo and Kababisa, increased throughput becomes unachievable and in turn, challenges the economics of the Lumwana expansion. While this scenario sounds extreme, it is not unimaginable given the cyclical nature of commodity prices, hence flagged as a risk by Mining Momentum. A minor risk of note is the small amount budgeted for closure, totalling US$175 M. While Mining Momentum has not been able to assess closure requirements of the project and the subsequent cost breakdown, by the end of mine life, two billion tonnes of ore would have been mined with at least four times that amount in waste; the actual closure cost is likely higher than the amount presented. However, this cost is incurred at the end of mine life, three decades into the future, resulting in a minimal impact on the overall project. Risk exists in any project, but Lumwana has both tonnes and grade. A decade has elapsed since the publication of the 2013 Technical Report and Lumwana continuous to grow. We find this kind of Reserve depletion and replenishment inspiring and Mining Momentum continues to believe that Lumwana will remain operational for many years to come, even outliving those that brought it to fruition!

The information presented above does not constitute investment advice. This is a summary from the NI 43-101 Technical Report effective December 31, 2024 (INSERT), with commentary from the author. Statements above do not represent the views of Barrick. If any discrepancies arise, the information contained within the NI 43-101 are official and final. For latest depletion data, please refer to the AIF update.