Jabal Sayid is copper, gold, and silver mine located in the Kingdom of Saudi Arabia, 350 km northeast of Jeddah. Jabal Sayid is a VMS deposit hosted in four mineralized lodes, consisting of felsic volcanic rocks cross-cut by hypabyssal intrusions within the Nuqrah Formation of the Arabian Shield. Jabal Sayid was discovered in 1965 by the Bureau de Recherches Geologiques et Minieres. Drilling in 1968 identified Lode 1, followed by Lodes 2, 3, and 4 in 1974. Further exploration was carried out, including an underground exploration program, culminating in a PFS that was completed in 1985, which concluded that the project was marginally economic. Teck re-evaluated the project in the late 1990s and conceptualized a large pit, but the project was not successfully funded. The Saudi state mining company Ma’aden was granted an exploration licence in 2000 and conducted further exploration but did not proceed. Through a number of takeovers, Jabal Sayid came under the sole ownership of Equinox Minerals, which was itself acquired by Barrick in 2011.

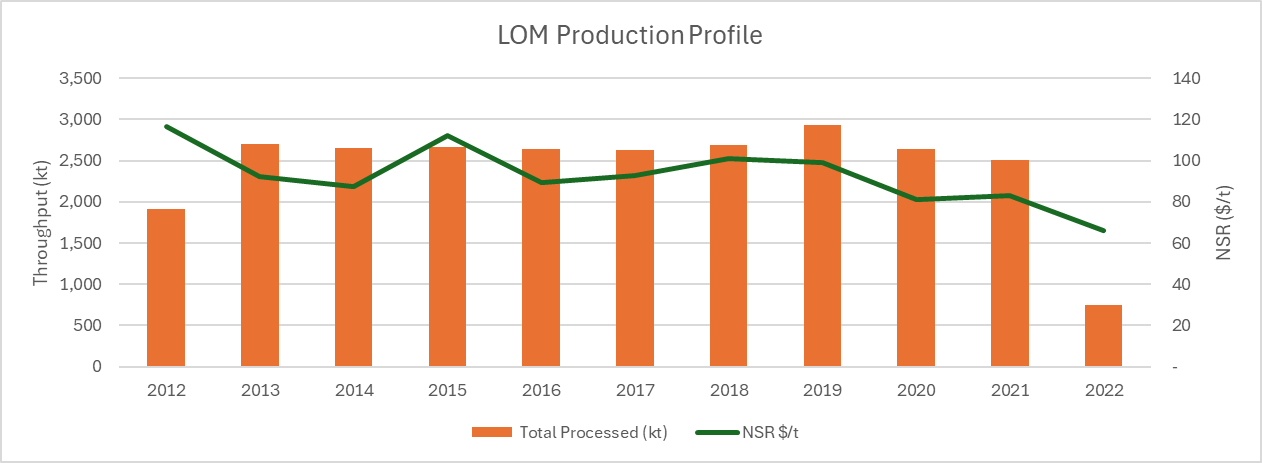

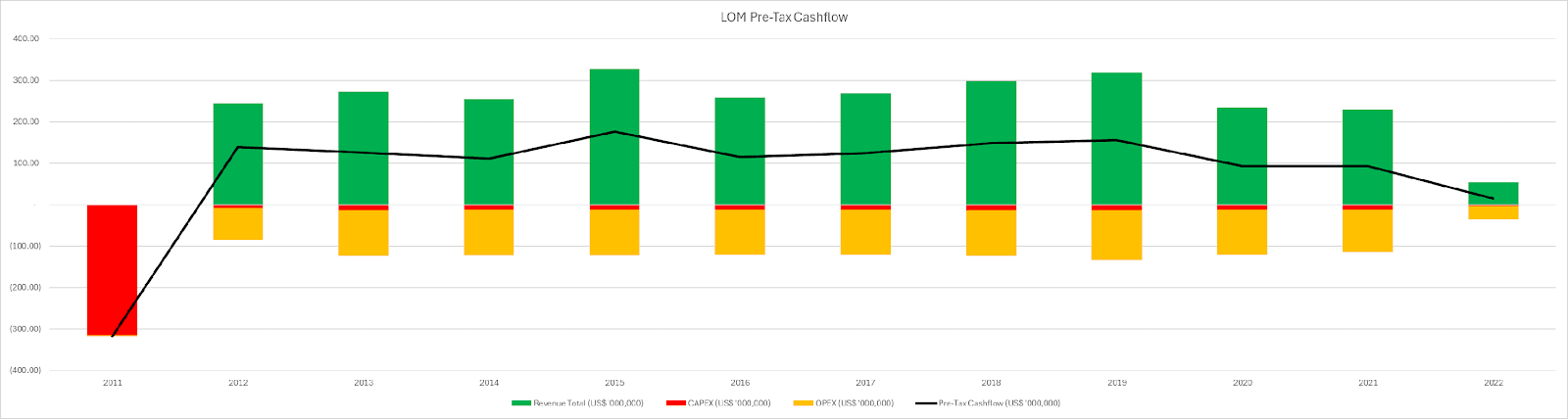

Jabal Sayid is planned as an underground mine using transverse Primaries-Secondaries longhole stoping with CRF to extract Lodes 2 and 4 at a rate of 2.6 Mtpa. The mine is expected to commence in 2011 with a two year ramp up period, concluding in 2022. The Life of Mine plan envisaged mining 26.7 Mt ore at 2.27% copper, 0.26 g/t gold, and 9.42 g/t silver, representing 57% Proven Reserve, 36% Probable Reserve, and the remaining 7% from Inferred Resources. A detailed financial model was not included in the Technical Report but using the Life of Mine plan in conjunction with the assumptions provided, Mining Momentum calculated a Pre-Tax Cashflow of US$824 M compared to the US$764 M presented. This discrepancy is likely due to unspecified payables and penalties. Mining Momentum assumed 97.5% gold, 70% silver, and 95% copper and no penalties.

| Tonnes (Mt) | Cu (%) | Au (g/t) | Ag (g/t) | Cu (M lbs) | Au (koz) | Ag (koz) | |

|---|---|---|---|---|---|---|---|

| Reserve | 24.4 | 2.20 | 0.25 | 8.80 | 1,183.6 | 196.1 | 6,904.2 |

| M+I | 4.2 | 3.55 | 0.72 | 12.30 | 329.0 | 97.1 | 4,410.9 |

| Inferred | 19.7 | 0.93 | 0.29 | 20.23 | 403.5 | 185.5 | 12,816.7 |

Jabal Sayid has a long history. Much has been done to define the deposit including an underground exploration program, but it has always remained marginal. The 2011 Technical Report demonstrates positive cashflow, yet a number of risks exist, some of which were identified by AMC in the Technical Report. AMC considered the mining rate achievable in thicker portions of ore with many primaries available in the earlier years of mining, but becomes increasingly challenging in narrower areas and secondary stopes in latter years of mine life. AMC also considered pastefill more appropriate than CRF for the scale of mining. On top of the risks identified by AMC, Mining Momentum considers the US$800k closure unrealistic. Adding US$20 M closure cost and removing 7% non-Reserve material results in a 25% reduction in Life of Mine cashflow. Mining Momentum also questions the sensibility of operating at over 7,000 tpd for a 10-year mine life, where 4,500 tpd over 15-years would appear more appropriate. Perhaps this decision was made with the assumption that Lodes 1 and 3 will come online by the time Lodes 2 and 4 are exhausted.

Currently no Reserve has been declared for Lode 1 and no Resource has been declared for Lode 3. 19.7 Mt of Inferred Resource grades at 1.06% CuEq with an additional 697 M lbs Zn contained. While copper grades in excess of 1% are attractive in the modern era, the issue is a lack of scale, less than 10 Mt assuming 50% conversion. An open pit concept has been floated, although feasibility is questionable. Mining Momentum is also unsure whether quantities of zinc are sufficient to justify an additional mill circuit. It is difficult to assess the potential of Jabal Sayid with the uncertainty of mining the upper portions of Lode 1 as open pit, the viability of zinc processing, and no information on Lode 3. Overall, Jabal Sayid is high in grade but limited in size. Historically, this rendered Jabal Sayid marginal, a fact that caused many to walk. Question is, do they regret it, now that gold and copper prices have reached all time highs or did they dodge a bullet?

The information presented above does not constitute investment advice. This is a summary from the NI 43-101 Technical Report effective March 7, 2011 (INSERT), with commentary from the author. Statements above do not represent the views of Barrick Gold. If any discrepancies arise, the information contained within the NI 43-101 are official and final. For latest depletion data, please refer to the AIF update.