Bulyanhulu is an underground gold, silver, and copper mine located in northwestern Tanzania, 155 km southwest of Mwanza and 55 km south of Lake Victoria. The deposit is situated in the Sukumaland Greenstone Belt, with mineralization hosted within steeply dipping, narrow vein quartz reefs within mafic volcanics. The structure extends 4 km along strike, 1 m to 5 m thick, from surface to 2 km deep. Gold was first discovered in the area in 1976 and was subsequently explored until Barrick acquired the property in 1999 and commenced commercial production in 2001. At the time of publication of the technical report, 9.6 Mt had been processed at a grade of 11.2 g/t, totalling 3.1 Moz gold produced.

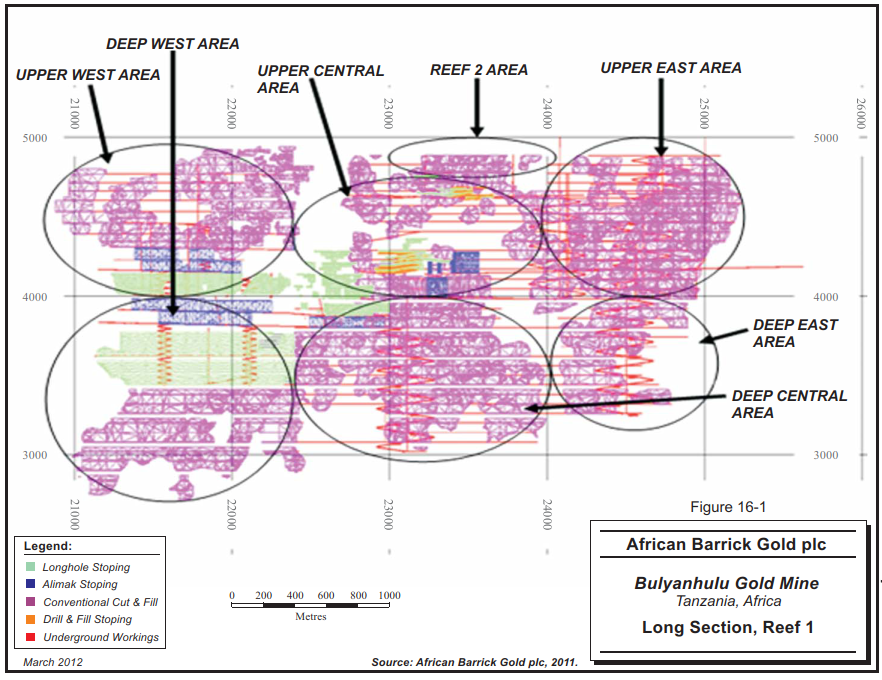

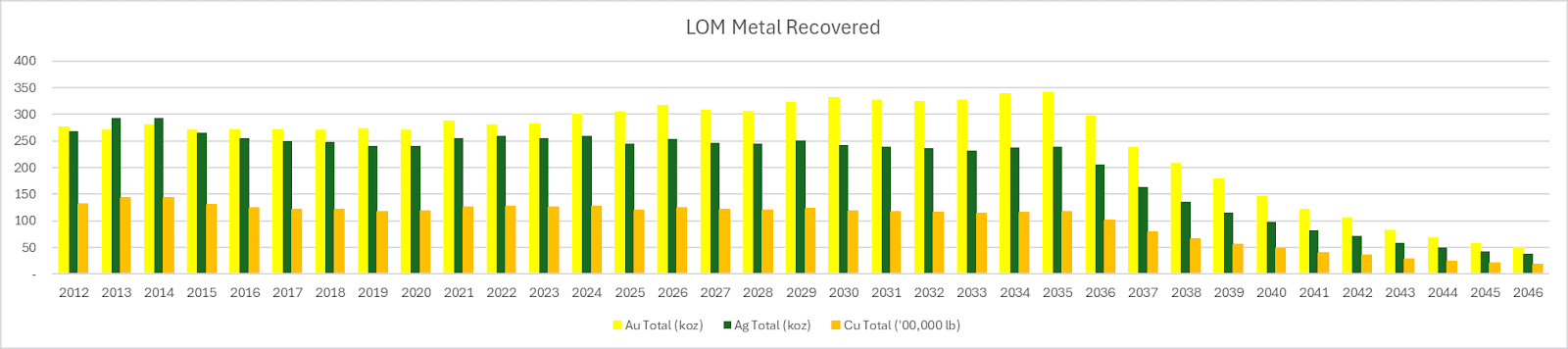

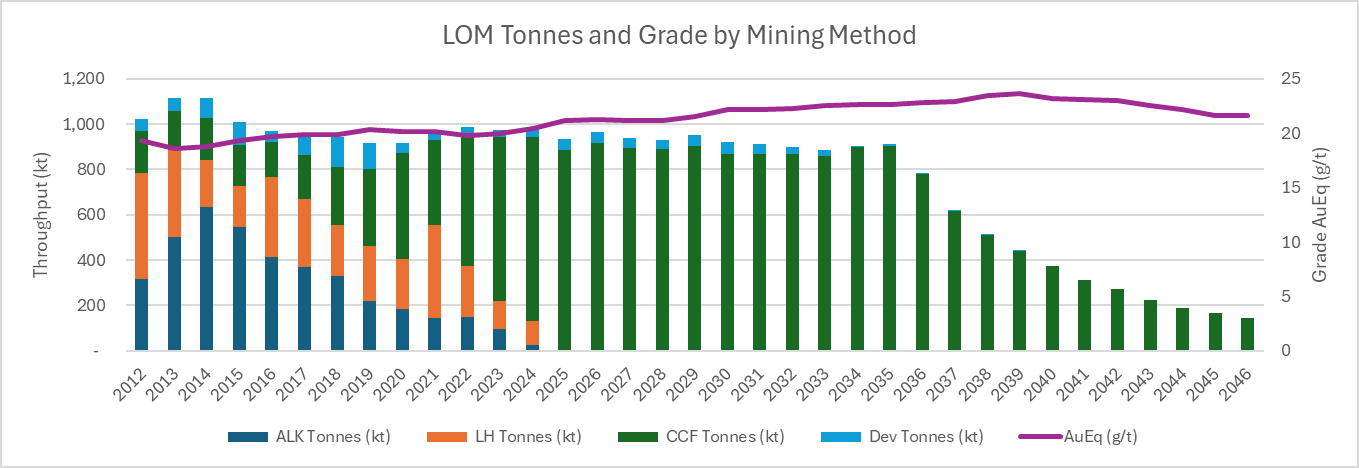

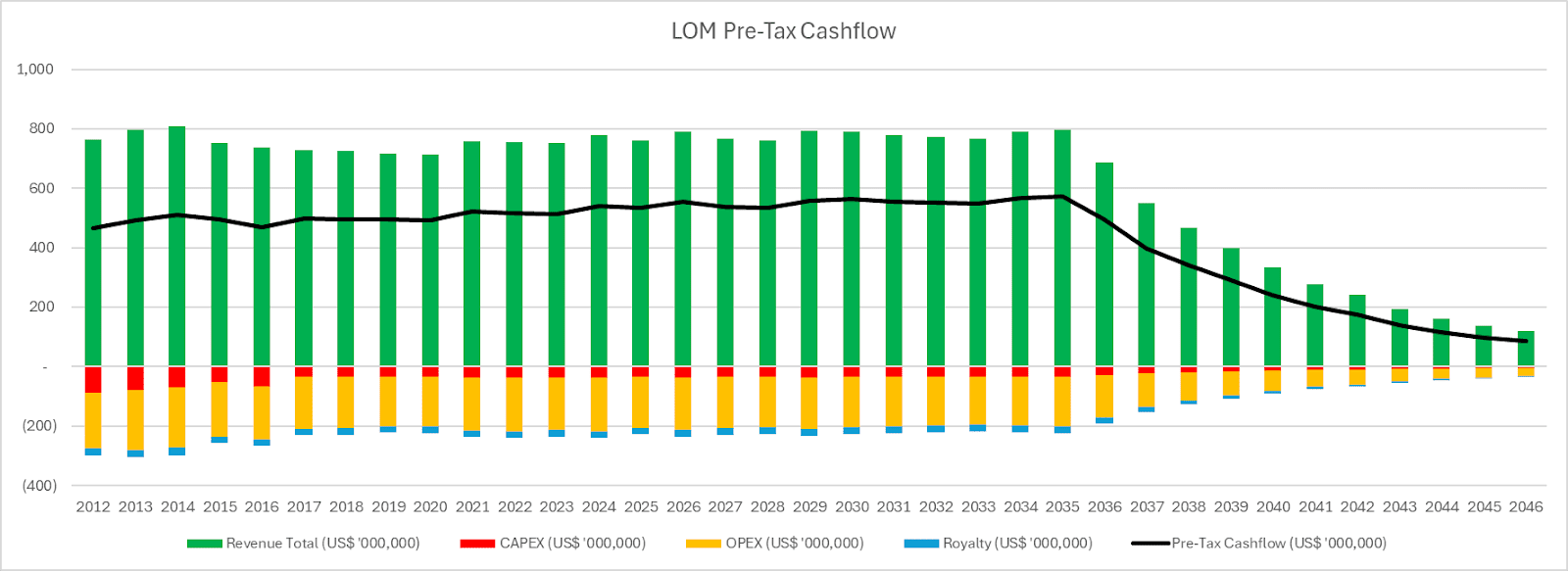

The underground mine is accessed via shaft and ramp. At the time of the technical report, the dominant mining method is longhole and alimak with a small proportion of conventional cut and fill. By 2020, cut and fill is supposed to make up half the mine throughput and by 2025, the sole mining method. Bulyanhulu is slated to sustain a throughput between 900 ktpa and 1 Mtpa until 2035, after which it tapers off until the end of mine life in 2046. No silver and copper grades have been included in the LOM plan in the technical report; Mining Momentum has estimated annual silver and copper production using constant values contained in the Reserve. Using a price of US$1,200/oz gold, US$28/oz silver, and US$3.25/lb copper contained in the technical report, Bulyanhulu produces in excess of 600 koz AuEq until 2035. As a producer, Bulyanhulu is under no obligation to disclose project economics. Based on 94% Mine Call Factor, 92.5% Recovery, OPEX of US$182/t, CAPEX of US$1,197 M, and 3% Royalty, Mining Momentum has estimated a Pre-Tax Cashflow of $15,150 M and US$4,733 M discounted 10%.

| Tonnes (Mt) | Au (g/t) | Ag (g/t) | Cu (%) | Au (koz) | Ag (koz) | Cu (M lb) | |

|---|---|---|---|---|---|---|---|

| Reserve | 28.2 | 11.73 | 9.39 | 0.67 | 10,632 | 8,506 | 416 |

| M+I | 17.8 | 5.28 | 4.33 | 0.31 | 3,018 | 2,474 | 123 |

| UG | 9.8 | 8.59 | 7.55 | 0.54 | 2,703 | 2,375 | 117 |

| Tailings | 8.0 | 1.23 | 0.39 | 0.04 | 315 | 99 | 6 |

| Inferred | 8.3 | 12.00 | 9.86 | 0.72 | 3,210 | 2,637 | 132 |

Bulyanhulu is one of those jackpot finds that builds companies into giants. It contains both tonnes and grade, sustaining high annual ounce production and long mine life. Exploration potential exists, with an additional 9.8 Mt underground M+I and 8.3 Mt in Inferred, likely extending mine life for at least another decade. An additional 8 Mt tailings is stockpiled, which becomes economical when gold price exceeds US$2,402/oz.

It is hard not to be dazzled by Bulyanhulu, but Mining Momentum has identified some risks below, which while not fatal flaws, must be carefully managed to maintain performance:

- Conventional cut and fill is labour intensive and low productivity. Bulyanhulu becomes increasingly reliant on this mining method, which carries risk of not delivering on plan and requires an increase in resource to support the desired mining rate. Mechanized cut and fill should be evaluated as an alternative.

- Cut and fill requires additional cement binder to expedite pastefill cure time, a substantial cost increase. Additionally, the effort required in backfill activities demands an increased number of backfill crews.

- Dilution estimates appear aggressive and is supported by reconciliation data, showing an additional 16% tonnes and -6% grade.

- Mining encounters increasingly challenging ground conditions at depth; cut and fill is a high exposure mining method and managing seismic ground increases cost and often results in production delays.

- Additional work is required to increase mill recovery from 91.1% (actual) to 92.5% (planned).

- G&A unit cost is high, largely due to the small number of tonnes processed. However, with reduced productivity in cut and fill mining, this number is likely to further increase.

Bulyanhulu is a true darling of a deposit, although moving to conventional cut and fill carries risk of increased cost and reduced mining rate, at over US$700/t revenue, there is plenty of margin to sustain cost increases. Grade hides all sins. With current commodity prices bringing in over US$1,000/t revenue, no one will bat an eye about costs so long as Bulyanhulu continues to produce ounces.

The information presented above does not constitute investment advice. This is a summary from the NI 43-101 Technical Report effective December 31, 2011 (INSERT), with commentary from the author. Statements above do not represent the views of Barrick Gold. If any discrepancies arise, the information contained within the NI 43-101 are official and final. For latest depletion data, please refer to the AIF update.