Hemlo is a gold camp located in northwestern Ontario, Canada 35 km east of the town of Marathon. The deposit is situated on the Schreiber-Hemlo greenstone belt, 3 km long, 2 km deep, 20 m wide, steeply dipping north, and plunging west. The property consists of the Williams Mine located in the western extent of the deposit, the formerly producing David Bell Mine in the centre, and the formerly producing Golden Giant Mine in the eastern extent. The area was first prospected in 1944 and by 1983, the potential size of the Hemlo deposit was clear to the three property owners at the time, Noranda (Golden Giant), Teck-Corona (David Bell), and Lac Minerals (Williams). Construction commenced at a breakneck speed and by 1985, all three mines entered production. As a result of Canada’s most famous lawsuit, Lac Minerals lost its Williams Mine to Teck-Corona. Through Homestake, Barrick came to own 50% of Williams and David Bell, eventually purchasing the remainder of Teck’s ownership stakes in 2009. In 2010, Barrick acquired Golden Giant from Newmont, making it the sole owner of all three properties. David Bell ceased production in 2013, having processed 9.9 Mt at a grade of 13.4 g/t, totalling 4.2 Moz gold and in the same year, Golden Giant ended production, having processed18.8 Mt at a grade of 11.5 g/t, totalling 6.9 Moz gold. At the time of publication, Williams remains the only operational mine, having produced a total of 11.4 Moz.

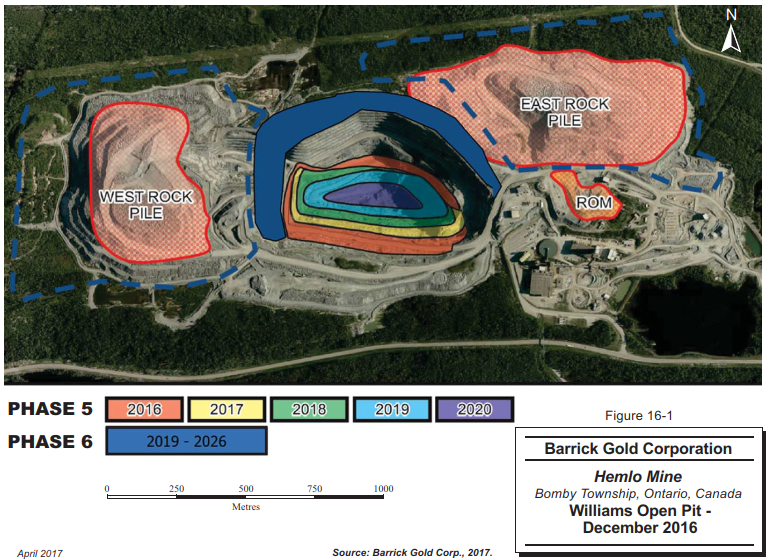

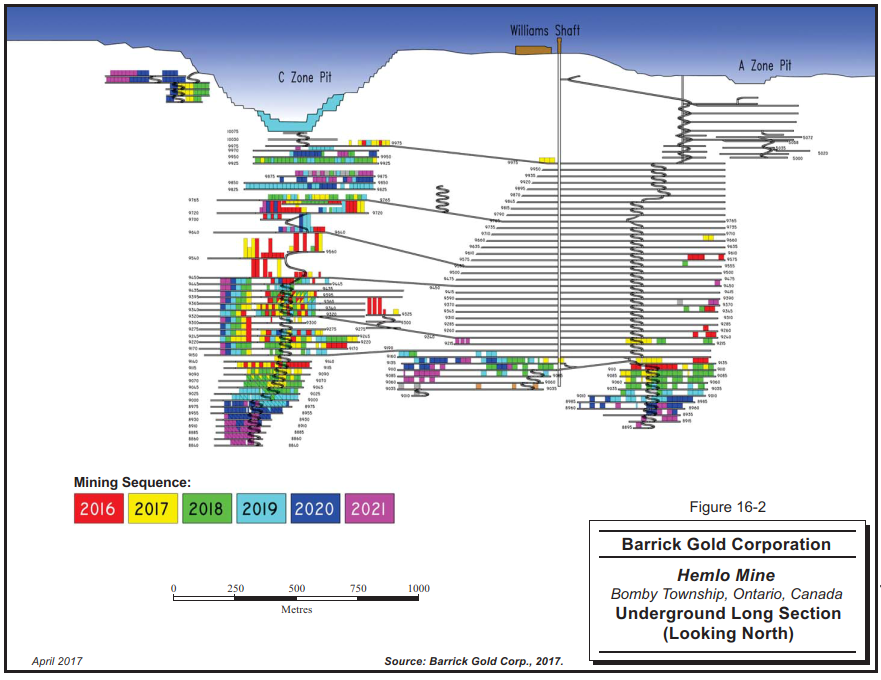

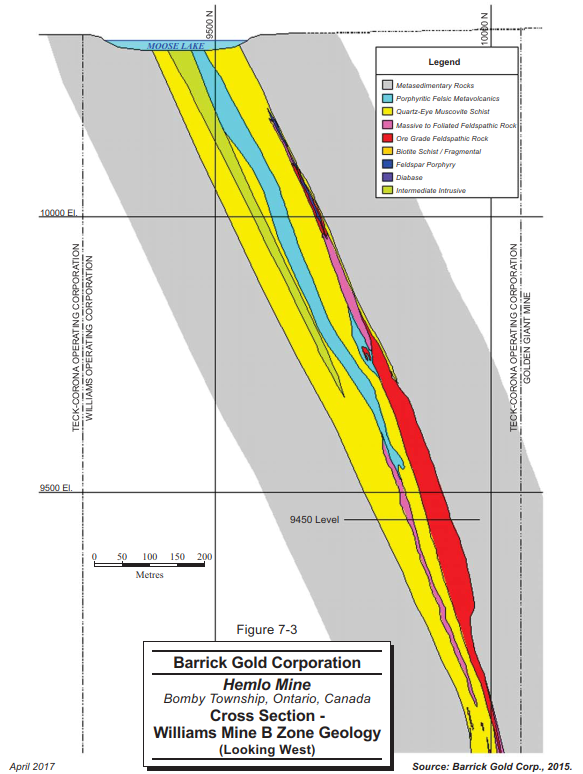

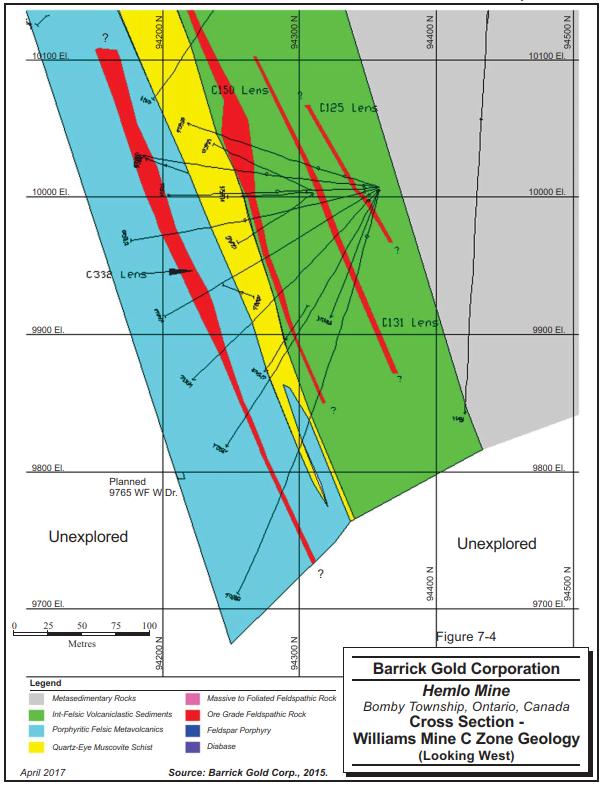

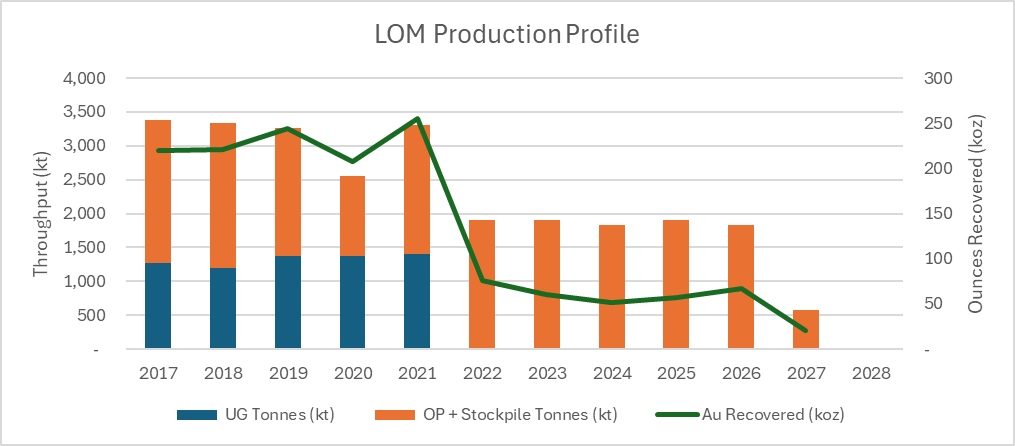

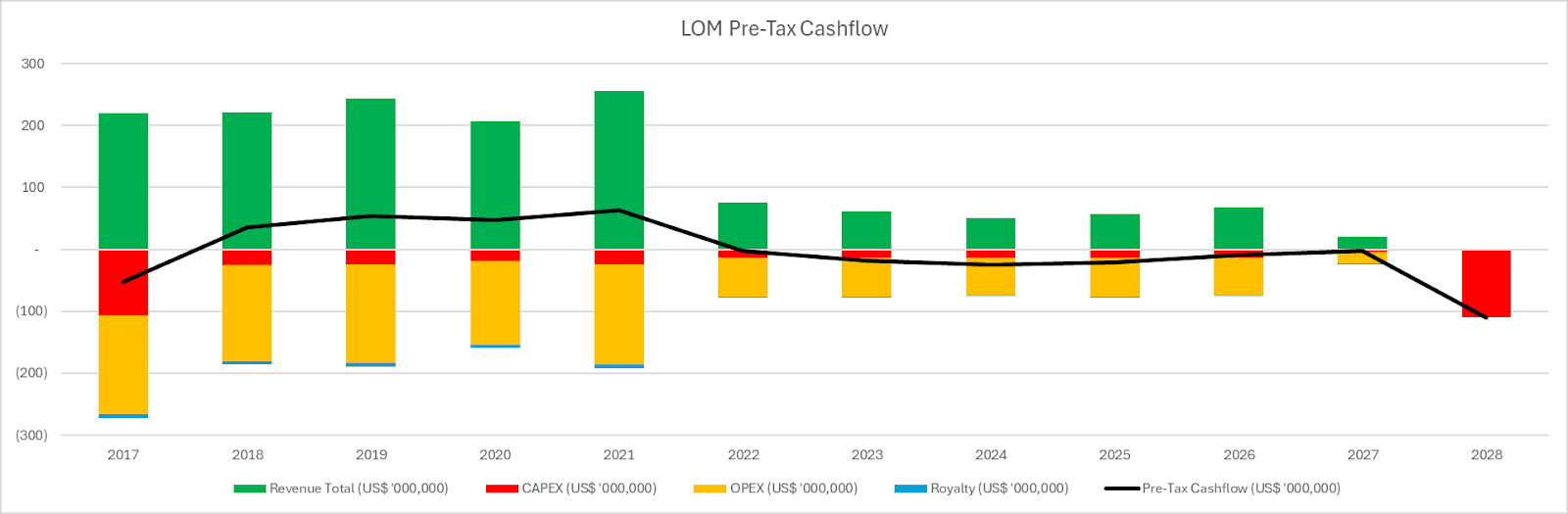

The Williams Mine consists of open pit and underground operations. The technical report presents new underground mining horizons in the Lower B-Zone, B-Zone West, C-Zone, and Sceptre. B-Zone ore is thick and continuous but tapers off at depth. C-Zone provides a new mining horizon, but the veins are relatively narrow. The deposit has a fairly small surface footprint, mined as a small open pit using conventional truck and shovel, with production planned until 2027. The underground is accessed via shaft and utilizes longhole and Alimak stoping. Alimak stoping allows for unlimited stope height and requires minimal lateral development, suitable for narrow vein, steep orebodies with little variation in dip. However, Alimak stoping is relatively expensive and requires long lead time. Combined operations have a planned throughput of 9,500 tpd until underground mining ceases in 2021. With simultaneous operations, Hemlo is expected to produce in excess of 200 koz per year with average LOM recovery at 93.3%. As a producing mine, Hemlo is under no obligation to disclose project economics. Mining Momentum has estimated project economics using the LOM plan and costs presented in the technical report to estimate a Pre-Tax Cashflow of US$(39) M and US$24 M discounted 10% using the Reserve gold price of US$1,000/oz and Pre-Tax Cashflow of US$515 M and US$407 M discounted 10% using a gold price of US$1,800/oz. This includes a CAPEX spend of C$275 M, LOM average operating cost of C$42.67/t open pit and C$91.54/t underground, and closure cost of C$110 M. With open pit only operations after 2021, unit costs for processing should increase due to reduced productivity and G&A should reduce due to reduced staffing needs.

| Tonnes (Mt) | Grade (g/t) | Contained (koz) | |

|---|---|---|---|

| Reserve | 25.8 | 1.92 | 1,588 |

| OP | 19.1 | 1.17 | 719 |

| UG | 6.6 | 4.08 | 868 |

| M+I | 58.9 | 0.91 | 1,720 |

| OP | 56.5 | 0.8 | 1,449 |

| UG | 2.4 | 3.49 | 270 |

| Inferred | 7.8 | 1.94 | 484 |

The Hemlo gold camp is legendary, producing over one million ounces of gold a year at its peak, playing no small part in creating the juggernaut that is Barrick. Needless to say, those glory days are long gone and an end is in sight for this deposit. Taking ownership of the Teck and Newmont properties has granted Barrick sole ownership of Hemlo, unlocking exploration to the west and downdip, material which has been presented in this technical report as new mining horizons. While this has been hailed as replenishing Reserves and Resources, Mining Momentum urges caution. The B-Zone tapers off at depth and C-Zone stopes are narrow, meaning productivity will likely reduce and costs increase. Open pit production is low, resulting in high costs. Viability as an open pit only operation appears questionable based on US$1,000/oz gold prices. While a large amount of tonnage sits in M+I Resources, these are mostly open pit. Mining Momentum urges caution as there is no mention of pit constrained Resources within the technical report; accounting for strip ratio, the amount of waste moved may render the material non-economical. Underground Resource is also fairly limited, offering approximately three more years of underground mining potential. The C-Zone is open at depth and offers exploration potential, a fact that the technical report emphasizes. Exploration to the west is particularly important, as in the opinion of Mining Momentum, Resources available for conversion to Reserves is limited and open pit operations after conclusion of underground mining is a risky economical proposition.

The information presented above does not constitute investment advice. This is a summary from the NI 43-101 Technical Report effective April 25, 2017 (INSERT), with commentary from the author. Statements above do not represent the views of Barrick Gold. If any discrepancies arise, the information contained within the NI 43-101 are official and final. For latest depletion data, please refer to the AIF update.