Pueblo Viejo is located in the Dominican Republic, 100 km northwest of the capital, Santo Domingo. Pueblo Viejo is an epithermal gold-silver deposit hosted in the Los Ranchos Formation, consisting of sedimentaries overlaid atop a volcanic basement, with quartz bearing facies interspersed. Gold mining occurred during Spanish rule and likely prior in the pre-Colonial era. Rosario Resources first explored the area in 1969 and undertook open pit mining of oxide material from 1975 until 1999, producing 5.5 Moz gold and 25.2 Moz silver. Subsequently, Eldorado Gold, Gencor (later Gold Fields), Mount Isa Mines, and Newmont carried out exploration and processing studies but no decisions were made to progress the project until Placer Dome purchased the site in 2001. Barrick acquired Placer Dome in 2006 and sold a 40% stake to Goldcorp, subsequently acquired by Newmont. Mine construction began in 2010 with commercial production commencing in 2013. At the time of publication of the technical report, Pueblo Viejo processed 175 Mt of ore to produce 9.7 Moz gold and 32.4 Moz silver.

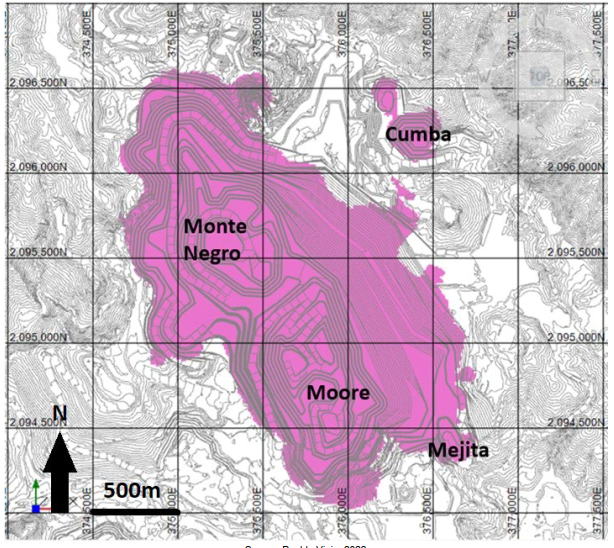

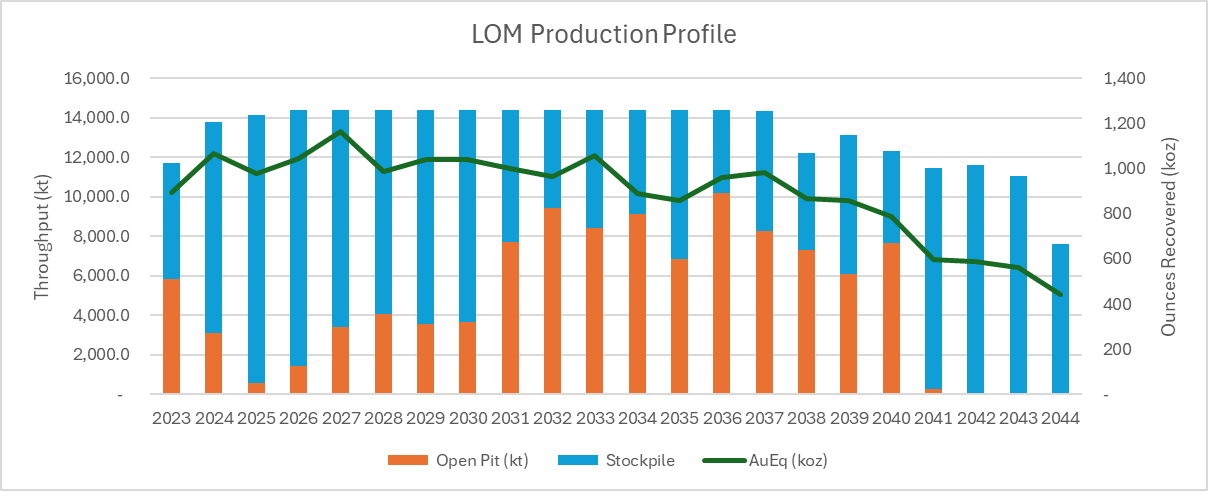

Pueblo Viejo is an open pit operation, consisting of two main deposits, Moore and Monte Negro along with satellite deposits, Cumba, Mejita, and ARD1. The open pit mines and stockpiles have a LOM strip ratio of just 1.8:1. Open pit mining uses conventional shovel and truck and expansion is underway to increase throughput to 14 Mtpa to produce 800 koz/year. Open pit mining is currently planned until 2041 followed by stockpile processing until 2044. LOM average recovery is 90.1% gold and 65.3% silver. As a producing mine, Pueblo Viejo is under no obligation to disclose project economics. Mining Momentum has used the LOM plan and costs presented in the technical report to estimate a Pre-Tax Cashflow of US$3.7 B (US$982 M Barrick’s share) and US$1.9 B (US$581 M Barrick’s share) when discounted 10% using the Reserve gold price of US$1,300/oz and silver price of US$18/oz. Note, Mining Momentum has not included the $1.26 B expansion capital spend since the project is near completion and may be considered a sunk cost. If this was included in our analysis, Barrick’s Pre-Tax Cashflow reduces to US$284 M with negative NPV.

| Tonnes (Mt) | Grade Au (g/t) | Grade Ag (g/t) | Contained Au (Moz) | Contained Ag (Moz) | AuEq (Moz) | Barrick’s AuEq (Moz) | |

|---|---|---|---|---|---|---|---|

| Reserve | 291.6 | 2.19 | 13.59 | 20.5 | 127.4 | 21.8 | 13.1 |

| OP | 196.1 | 2.19 | 12.87 | 13.8 | 81.1 | 14.7 | 8.8 |

| Stockpile | 95.4 | 2.17 | 15.10 | 6.7 | 46.3 | 7.1 | 4.3 |

| M+I | 196.9 | 1.83 | 11.53 | 11.6 | 73.0 | 12.3 | 7.4 |

| OP | 196.9 | 1.83 | 11.53 | 11.6 | 73.0 | 12.3 | 7.4 |

| Inferred | 7.6 | 1.80 | 10.50 | 0.4 | 2.6 | 0.4 | 0.3 |

It goes without saying that Pueblo Viejo is an incredible deposit, with certain years exceeding 1 Moz gold equivalents. Even just processing stockpile in the final years of mine life, it still manages to achieve the coveted 500 koz to be classified as Tier 1. It has high tonnes, high grade, and minimal waste movement. The problem is how good of a deposit Pueblo Viejo is and everyone knows it. Firstly, 40% is owned by Newmont. Then there are 3.2% NSR and 28.75% NPI paid to the local government. Finally, there is the stream on Barrick’s share, where Royal Gold pays 30% of the price for 7.5% gold ounces up to 990 koz, then 3.75% and 75% silver ounces up to 50 Moz, then 37.5%. This removes $1.2 B from Barrick’s Pre-Tax Cashflow of US$2.2 B. In fact, the reduced rates do not come into effect over the duration of the LOM. Royal Gold paid US$610 M for this stream which is worth $534 M after 10% discount so they must have been bullish on gold prices and/or Life of Mine extension. Mining Momentum is confident in both; a US$1,300/oz Reserve price is far below spot price and Pueblo Viejo sits atop a massive Resource of 7.4 Moz M+I, which if feasible, can add over a decade of mine life. Furthermore, the deposit is open at depth and underground options have yet to be explored. There is truly no end in sight for mining at Pueblo Viejo, we have just scraped the surface.

The information presented above does not constitute investment advice. This is a summary from the NI 43-101 Technical Report effective December 31, 2022 (INSERT), with commentary from the author. Statements above do not represent the views of Barrick Gold. If any discrepancies arise, the information contained within the NI 43-101 are official and final. For latest depletion data, please refer to the AIF update.